The inflation data received in the current week fed precisely those concerns and emerging fears of an even significantly stronger inflation among a growing number of market players and observers. Let’s just look at the bare figures in the U.S. and the People’s Republic of China.

US-Consumer Price Data Significantly Exceed Analysts Expectations

Naturally, the release on the development of U.S. consumption and consumer prices in the month of May was eagerly awaited in many places. The figures announced today by the Bureau of Labor Statistics definitely add fuel to growing concerns about a significant rise in inflation among an increasing number of observers and market players.

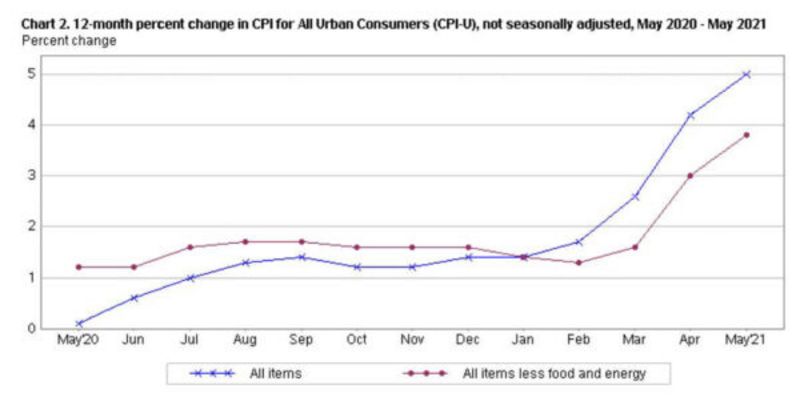

For example, the consumer price index (CPI) in the United States rose by 0.6 percent on a monthly basis in May. Consensus estimates made in advance, among analysts and economists who on average had expected an increase of “only” 0.4 percent, were thus clearly missed.

Compared with the same period of the previous year, the CPI jumped to a full five percent in May (after 4.2 percent in the previous month). Consensus estimates among analysts and economists had anticipated an annualized increase in U.S. inflation to 4.6 percent in advance of the data release. This estimate was also exceeded by a wide margin.

Highest inflation rate since 2008 – core consumer prices is also rising unexpectedly fast

Fed Chairman Jerome Powell, who still describes the current price trend in the United States as “transitory”, could soon find himself in greater need of explanation, as this is now the highest inflation rate in the United States since August 2008.

Since January of this year, the consumer price index in the United States has been moving steadily upward. On the so-called core consumer price front, things did not look promising at all in the month of May either.

Rather, core consumer prices climbed 0.7 percent compared to April, while analysts and economists estimated a monthly increase of 0.4 percent.

Over the past twelve months, core consumer prices in the U.S. have skyrocketed to 3.8 percent. Consensus expectations were for 3.4 percent before the data were published.

Goods and services prices with enormous increases

Although it must be taken into account that this was a relatively low starting point in view of the month of May last year, there is no hiding the fact that this is the strongest annual increase in US inflation since June 1992.

While goods prices in the U.S. rose a solid 6.5 percent on an annual basis in the month of May to their highest level since 1982, service prices also rose significantly over the same period.

As BLS data released further show, price increases in new vehicles, used vehicles, trucks, furniture furnishings, textiles and apparel, home furnishings, as well as airfare and travel costs continued in the month of May. Medical goods were among the few subindices that fell slightly.

Vehicle and air travel sectors particularly affected

Developments in the used vehicle sector (cars and trucks) stood out especially in the month of May. Prices in this sector rose again last month, by 7.3 percent.

New vehicles also became 1.6 percent more expensive in the month of May, which equates to the strongest increase on a monthly basis since October 2009. Air travelers also had to pay higher prices, following a renewed rise in ticket prices of a whopping seven percent in May (versus +10.2 percent in April).

Prices in the rental car sector (cars and trucks) also increased by 12.1 percent in May (after 16.2 percent in April). Over the past twelve months, vehicle rental prices in the United States have thus more than doubled.

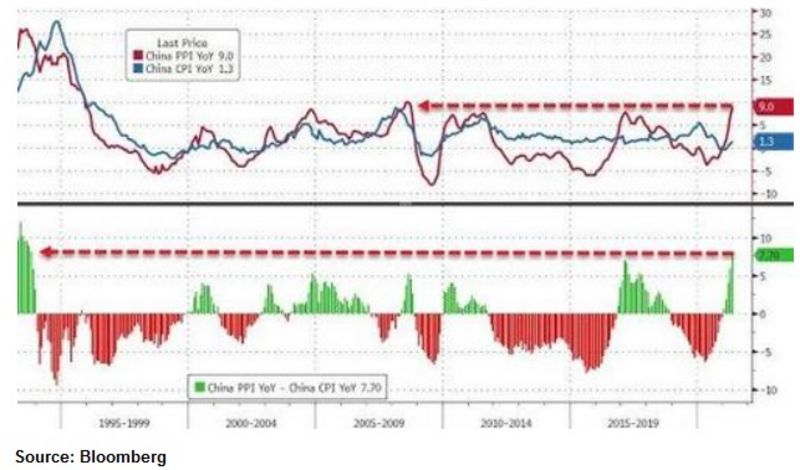

Producer price increase in China at financial crisis level

The publication of producer prices in the People’s Republic of China had already caused a shocking atmosphere in last weeks trading. The inflation among local producers in the Middle Kingdom climbed to 9 percent in the month of May due to raw materials, some of which have risen sharply in price – only just below the former all-time high.

This was also the highest producer price inflation since the financial crisis, or more precisely since September 2008, the month of the Lehman collapse.

At the same time, the difference between the Chinese consumer price index and producer prices in the People’s Republic of China, which is being closely watched in some quarters, widened once again – to its highest level since 1993.

It is obvious from these charts that the United States is likely to face import prices, which are likely to rise significantly, as most products sold in the U.S. are manufactured and imported from china due to the outsourcing of factories and jobs to the Middle Kingdom, which has been going on for 30 years by now.

What might an intervention by the People’s Bank of China look like?

If producer prices in the People’s Republic of China rise even more sharply in the coming months, not only can falling profits among Chinese producers – due to declining demand in many areas – be forecasted, but new interventions by the People’s Bank of China could also occur again soon.

The People’s Bank of China could intervene to try to import as little inflation into its own country as possible. About two weeks ago, Beijing’s leadership had already indicated that it wanted to take action against rising commodity prices – even though since then almost everyone seems to be asking themselves in what way such a goal should be achieved and how such a move could be accomplished.

To hit the brakes on the inflation front, the People’s Bank would likely have little choice but to tighten domestic financial and credit market conditions even more than at present and/or raise its own base rate.

As far as the domestic market is concerned, many Chinese producers do not (yet) seem to have widely passed the price increases to their own consumers. This assumption can be gauged, for example, from the Chinese consumption and consumer price index, which is still stuck at just 1.6 percent.

Bank of America warned of “temporary hyperinflation” as early as the beginning of May

It should be noted that the Bank of America had already pointed out at the beginning of May that inflation in the United States was likely to rise sharply.

At that time, the major U.S. bank said that there could even be “temporary” hyperinflation in the United States. Leading analysts of the bank derived their conclusion, among other things, from telephone analyst conferences in the corporate sector.

During these analyst conferences, they said, mentions of the term “inflation” have recently increased significantly. In the third week of the reporting season, the use of the term “inflation” had even increased by four hundred percent compared to the same period of the previous year – to climb by almost eight hundred percent in the following reporting weeks.

Pre-indicator: Food inflation in emerging markets and developing countries on the rise

According to Bank of America, this is the highest measured value since 2011, a year we still remember well – the year in which commodity prices exploded, which in turn contributed to social unrest in emerging and developing countries as well as the Arab Spring.

Consumers in the traditional industrialized countries are not yet feeling the effects of rising prices as strongly as the emerging and developing countries. However, I have to be a little cautious with this statement, since a quadrupling of wood prices, for example, has already led to enormous increases in construction costs (by up to $40,000 more per property).

Nevertheless, food inflation in emerging and developing countries in particular often kicks in much earlier than in Europe or the United States. This is already the case in many nations on the African continent, which means that more and more families are finding it increasingly difficult to make ends meet financially.

In Europe, even doubling tomato prices could still be accepted by most families, but this is not the case from the perspective of many African countries.

Of concern is the fact that even the consumer price index in the United States – which has been statistically manipulated from top to bottom – now seems to be rising sharply. There are also a great many financially less well-off residents in America who were already having a hard time making ends meet before the covid crisis broke out.

The Biden administration is still providing generous government benefits to some of the unemployed in the U.S., but everyone knows that this situation will not last forever – especially since a growing number of U.S. companies are beginning to complain that they can no longer recruit workers because of this very circumstance.

DepthTrade Outlook

Whatever official sources report on future inflation developments, it is advisable to look at the actual data – i.e. the regional consumer and producer price indices. After all, neither any authorities nor Fed Chairman Jerome Powell have a crystal ball to look into the future. Therefore, all the talk about “temporary” inflation seems to be based on the hope of keeping the financial markets – especially the bond markets – happy.