It is obvious that rising energy prices, inflation, and possible interest rate hikes on the one hand and economical growth slowdowns and the risk of rising infection rates in the coming winter (and thus new restrictions) on the other significantly increase the probability for stagflation.

What exactly is “stagflation”?

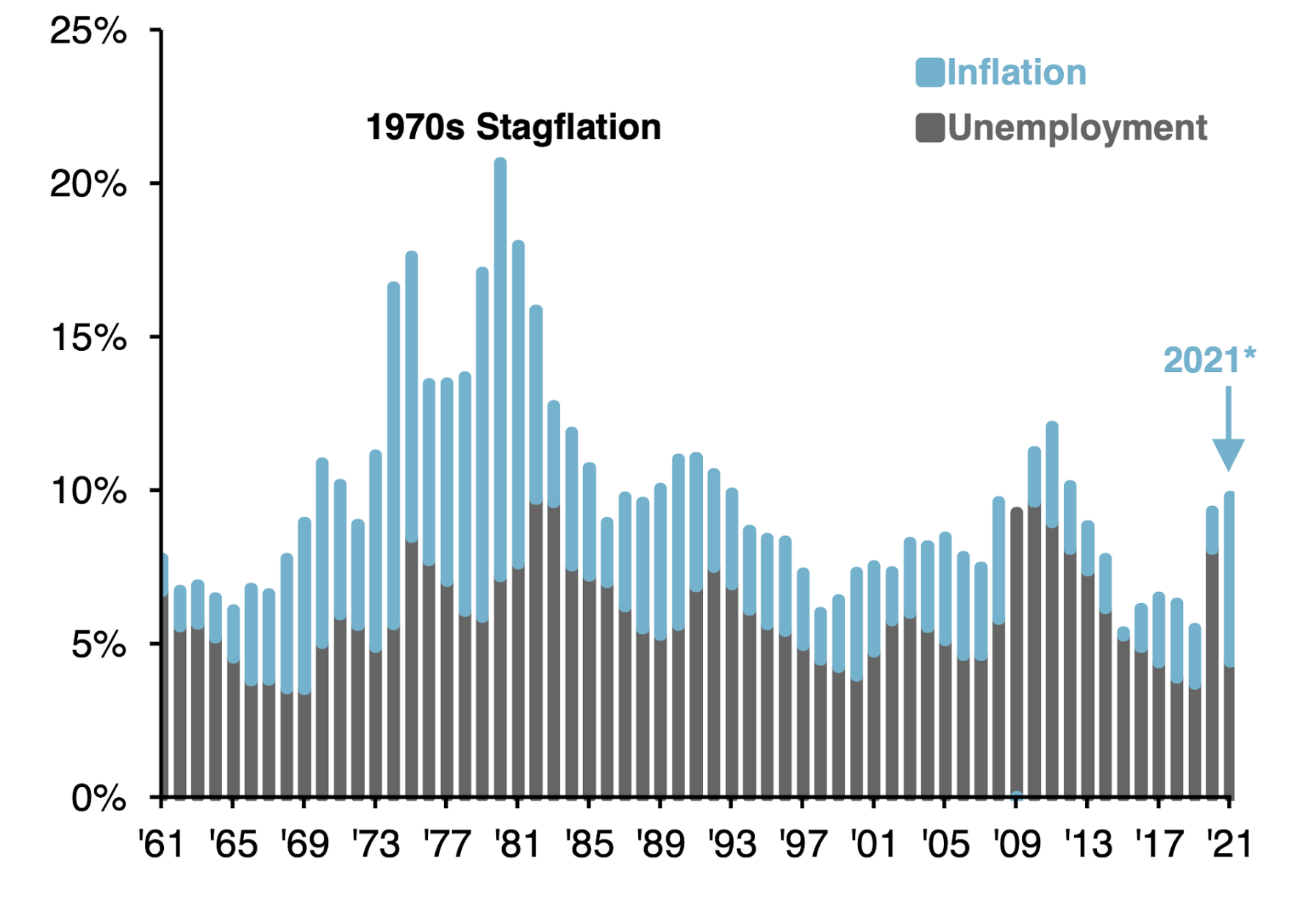

The term stagflation was created in the 1970s and is a combination of the economic terms stagnation and inflation. It refers to the simultaneous occurrence of stagnation (i.e. the absence of growth) and inflation (i.e. an increase in prices or currency devaluation). Stagflation usually also leads to rising unemployment and declining prosperity.

In stagflation, economic policy is in a quandary: If the government cuts taxes to boost growth, inflation also continues to rise. If, on the other hand, the central bank raises interest rates to curb inflation, economic growth declines even further.

A starting point is usually an unexpected event (like the coronavirus pandemic) that weakens economic growth while fueling inflation. Example: In the 1970s, political tensions arose as a result of which OPEC, the Organization of the Petroleum Exporting Countries, severely curtailed its oil production.

The reduction in supply drove up the price of oil sharply. This oil price shock had far-reaching consequences in the Western industrialized countries – among other things, production costs rose. This in turn resulted in higher prices for products. At the same time, however, their own production was curtailed.

Inflation rose significantly, but at the same time, economic growth stagnated. Consumers were therefore no longer able to push through higher wages, many lost their jobs, and prices rose nonetheless. Consumers had to cope with higher prices on a stagnating salary. Demand thus fell – companies had to cut production even further.

2021/2022

As energy prices continue to rise and supply constraints persist, the pressure on central banks to respond with interest rate hikes at some point is increasing. Certainly, central banks have to look through temporary factors of inflation. But whether inflation will soon fall again as the special effects run their course, as many expect, or whether it will prove more stubborn after all and remain permanently elevated, we will not know with some certainty for several months.

However, possible interest rate hikes could put the brakes on growth again. In addition, it is difficult to predict whether the next wave of viruses is on the way (presumably yes), how it will develop, and what impact it could have on economies. Certainly, after a year and a half of pandemic, businesses and service providers have largely adapted to the new circumstances. But still, despite high vaccination rates, the rising infection rates again carry a certain residual risk of new restrictions and disruptions in economic processes, after all, the virus is still a deadly danger for older people with pre-existing conditions, a fact brought to the fore again by the death of (vaccinated) former U.S. Secretary of State Colin Powell.

It is conceivable that, against this backdrop, market concerns about a possible stagflation scenario could intensify, with a corresponding increase in uncertainty and instability. In such a scenario, the currencies that could emerge most unscathed are those in which infection rates are rising or even falling the slowest, and whose central banks can credibly communicate their monetary policy without giving the impression that they might be behind the curve (i.e., not responding sufficiently to inflationary threats) or too active (thus increasing the risks of an economic slowdown). The market is therefore likely to visibly tap the economic data for corresponding signals of impending stagflation.

Currently, there is evidence in favor of the U.S. dollar, including the upcoming start of tapering, which is why it may well gain in the coming weeks and months. In the medium term, however, things could look different again and the market could adjust its view. Depending on how the inflation and infection rates and the economic data develop.